Press Release

Indian Housing Affordability Likely to Stabilise This Year as Household Income Growth Set to Outpace Property Price Appreciation

March 26, 2026

National, March 26, 2026: The affordability of homes in India's top cities is expected to be stabilised between 2026 to 2028 on the back of rising household incomes and favourable policy interventions, according to the CBRE Housing Affordability Index released by real estate consultancy CBRE South Asia Private Ltd.

The consultancy highlighted these findings in its India Residential Market Outlook 2026, evaluating the EMI-to-household income ratio across six major cities and three income brackets from 2021 to 2028. It signalled that for the first time since 2021, household income growth is now anticipated to outpace property price appreciation, easing the homebuying burden for a wide range of Indian households. This growth is likely to align with the country's transition to upper-middle-income status by 2030[1] and policy momentum amid geopolitical uncertainties.

"India's housing market is at a structural inflection point," said Anshuman Magazine, Chairman & CEO, India, South-East Asia, MEA, of CBRE. "The convergence of monetary easing, moderating price appreciation, and rising household disposable incomes is expected to cushion homebuying conditions across cities and income segments. The sector could witness a divergence in sales value-over-volume dynamics in 2026."

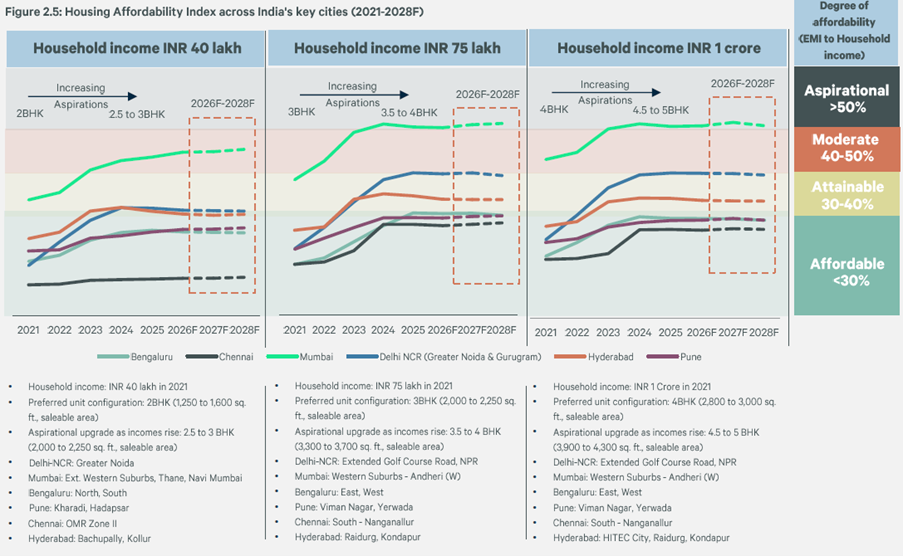

The report tracked affordability across three annual household income brackets—INR 40 lakh, INR 75 lakh, and INR 1 crore—across Mumbai, Delhi-NCR, Bengaluru, Hyderabad, Chennai and Pune, mapping the EMI burden against evolving aspirations of homebuyers from 2021 to 2028.

It recorded a consistent upward movement in the EMI-to-income ratio across all three cohorts between 2021 and 2024. This can be attributed to the Reserve Bank of India's interest rate-tightening cycle and to capital value growth outpacing household income gains.

However, the index signals a definitive pivot from 2026 onwards. Across all three income cohorts, the EMI-to-income ratio is projected to plateau between 2026 and 2028, pointing to a measurable stabilisation in homebuying affordability through the forecast period. This stabilising trajectory is reflected across distinct buyer segments and micro-markets.

[1] SBI Research, January 2026

Source: CBRE Research**

Gaurav Kumar, Managing Director & Co-Head, Capital Markets and Residential Services, India, CBRE, said, "The market is anchored by a resilient growth baseline and disciplined supply-demand parity. The anticipated stabilization in affordability over the next three years will be a vital catalyst in sustaining this momentum and informing strategic capital objectives across the ecosystem."

Residential market snapshot: 2025 in review

CBRE Research further noted that India's residential sector recorded new launches and sales exceeding 270,000 units each in 2025. The high-end segment captured about 27% share of total sales, eclipsing the mid-end bracket for the first time. Premium and luxury sales grew over 30% year-on-year. The supply, at the same time, grew 38% Y-o-Y with approximately 52,000 luxury units launched during the year.

Importantly, while sales volume moderated by approximately 8%, sales value grew approximately 15%. It underscores the market's structural shift toward better quality and higher-ticket inventory.

Affordable housing: Policy recalibration needed

CBRE Research also flagged a divergence within the affordable housing story; the sub-INR 45 lakh affordable segment remains constrained due to elevated input costs and the withdrawal of targeted fiscal incentives.

A strategic government-led recalibration, specifically through the reassessment of price and area ceilings and the reinstatement of targeted incentives for both developers and end-users, may help restore the segment's market share to pre-COVID levels of 25–30%. According to the report, this could potentially add around 60,000 new annual units to the pipeline.

* Definition of segments as per ticket size (INR) for Mumbai & Delhi -NCR: Affordable - up to 45 lakh; Budget - 45 lakh-1 crore; Mid-end - 1-1.5 crore; High-end - 1.5-3 crore; Premium- 3-6 crore; Luxury - 6-50 crore and Ultra Luxury - 50 crore and above. For Bengaluru & Hyderabad: Affordable – up to 45 lakh; Budget 45-75 lakh; Mid-end - 75 lakh-1.5 crore; High-end - 1.5C-2.5 crore; Premium - 2.5-5 crore; Luxury - 5-50 crore and Ultra Luxury – 50 crore and above; for Pune, Chennai &Kolkata: Affordable - up to 45 lakh; Budget - 45-75 lakh; Mid-end – 75 lakh-1.25 crore; High-end - 1.25-2.5 crore; Premium - 2.5-4 crore; Luxury - 4 crore and above

** For households earning INR 40 lakh annually - typically targeting 2BHK configurations in micro-markets such as Greater Noida, Thane, Navi Mumbai, Bengaluru North and Hyderabad's Bachupally-Kollur corridor - the EMI-to-income ratio is expected to plateau, bringing homes in the INR 1.25–2 crore range increasingly within reach.

For the INR 75 lakh cohort - targeting 3BHK units across Bengaluru East and West, Pune's Viman Nagar, Chennai South and Hyderabad's Raidurg-Kondapur belt - affordability is transitioning from "moderate" to "attainable" on the index scale.

For INR 1 crore earners typically pursuing 4BHK premium configurations across locations like HITEC City, Golf Course Road extensions and Mumbai's Western Suburbs, the index points to a measurable easing of the EMI burden through the forecast period.

CBRE Group, Inc. (NYSE:CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage serving, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, digital infrastructure services); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.

CBRE was the first International Property Consultancy to set up an office in India in 1994. Since then, the operations have grown to include more than 13,000 professionals across 15 offices, with a presence in over 100 cities in India. As a leading international property consultancy, CBRE provides clients with a wide range of real estate solutions, including Strategic Consulting, Valuations/Appraisals, Capital Markets, Advisory & Transactions, Global Workplace Solutions & Property Management, and Project Management. The guiding principle at CBRE is to provide strategic solutions that make real estate holdings more productive and economically efficient for its clients across all service lines. Please visit our website at https://www.cbre.co.in/