Press Release

Mumbai tops real estate equity investments with USD 6.9 bn between CY 2022-24, highest in India: CBRE-CII Report

April 22, 2025

Mumbai – 22nd April 2025 – CBRE South Asia Pvt. Ltd., India’s leading real estate consulting firm, announced the findings of its joint report with Confederation of Indian Industry (CII) titled, ‘Bricks & Billions – Mapping the Financing Landscape of Real Estate’. The report was released in the presence of Rishi Kumar Bagla, Chairman, CII Western Region and Chairman & Managing Director, BG Electricals and Electronics, Rami Kaushal, Managing Director, Consulting & Valuation Services, India, Middle East, Africa, CBRE and Nikhil Bhatia, Managing Director and Co-Head, Capital Markets, CBRE India.

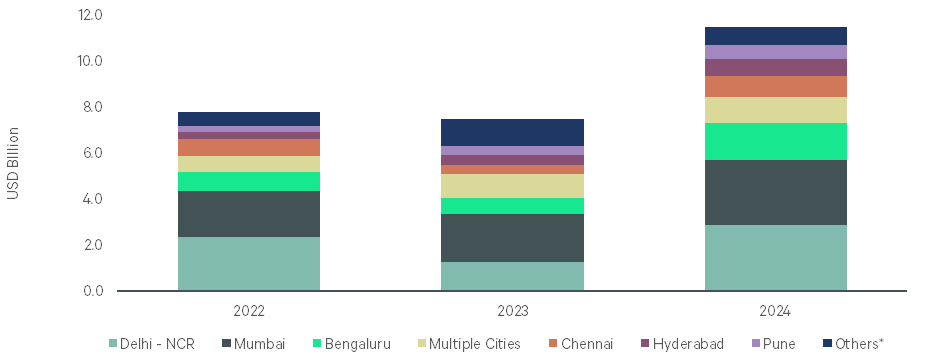

The CBRE – CII joint report provides a view of real estate landscape and prevailing financing strategies, including those pertaining to real estate equity and debt investments and AIFs, among other strategic insights. According to the report, Mumbai topped the real estate equity investments with the highest inflows of USD 6.9 bn, accounting for a ~26% share in the total real estate equity investments between CY 2022-24. Together, Mumbai, Delhi-NCR, and Bengaluru attracted around USD 16.5 bn, accounting for a cumulative 62% share during this period. This sustained dominance of gateway cities was driven by a high concentration of investment-grade projects, robust urban infrastructure, a skilled talent pool, strong demand across asset classes, and a steadily formalising real estate ecosystem. Land/developments sites attracted the largest share of equity investments, accounting for a 44% share of total inflows between CY 2022-24, followed by built-up office assets, which had a 32% share. Total real estate equity investments during CY 2022-24 stood at USD 26.7 bn in India.

Between CY 2022 and 2024, tier-II cities accounted for nearly 10% of total real estate equity investments, amounting to approximately USD 3 bn. During this period, land/developments sites emerged as the leading investment sector in tier-II cities, attracting approximately 47% share of the total tier-II capital inflows, followed by the industrial and logistics (I&L) sector, which accounted for an around 25% share. Sustained economic momentum in tier-II cities, driven by rapid industrialisation, rising consumption, and expanding infrastructure, have positioned them as attractive destinations for investors.

City-wise split of equity inflows (CY2022-CY2024)

*Others include – Kolkata, Ahmedabad, and tier-II cities such as Nagpur, Cuttack, Ludhiana, Mohali, Lucknow, Panipat, Sonipat, Nashik, etc.

Anshuman Magazine, Chairman & CEO - India, South-East Asia, Middle East & Africa, CBRE, said, “India’s real estate sector is entering a new phase of growth, powered by robust capital inflows and a significant pool of dry powder ready for deployment. The strong investor sentiment, especially in built-up office assets and residential developments, is underpinned by sound fundamentals and steady end-user demand. We believe this momentum will sustain as India’s structural reforms and corporate evolution continue to attract long-term capital.”

Rishi Kumar Bagla, Chairman, CII Western Region and Chairman & Managing Director, BG Electricals and Electronics, said, “India’s real estate sector is rapidly institutionalising, creating a more transparent, risk-mitigated environment that aligns with global investor expectations. Enhanced due diligence frameworks, sustainable development mandates, and stronger compliance protocols are becoming the norm. With 1 in 5 investors prioritising green buildings, ESG-led investment strategies are no longer optional—they are central to long-term value creation. As the sector becomes more structured and regulated, we expect deeper participation from global funds, especially those focused on sustainability and resilience."

Rami Kaushal, Managing Director, Consulting & Valuation Services, India, Middle East, Africa, CBRE, said, “The next wave of real estate investment in India will be defined by the growth of alternate sectors—data centres, healthcare, hotels, education, student housing, and co-living spaces. These segments are benefiting from digital acceleration, changing urban lifestyles, and favourable government policies. With land acquisition and platform-level investments already gaining traction, we anticipate increased investor interest in these future-ready asset classes. The market is clearly maturing beyond traditional sectors, offering diversified, innovation-led opportunities for both domestic and international capital.”

Outlook and Other Observations

Key Themes Likely to Influence the Sector (Short to Mid-Term)

1. Public Equity Market Potential: Public equity markets are expected to remain active in 2025. The anticipated listing of another major REIT in the year signals sustained investor appetite for stable, income-generating real estate assets. This would further deepen the REIT market, offering more avenues for capital inflows and potentially attracting a wider range of investors.

Multiple leading flexible space operators are also expected to file for public listing in 2025, underpinning sustained demand from large enterprises and startups across sectors and geographies.

2. Lower Financing Costs: The RBI’s shift in stance from 'neutral' to 'accommodative' signals a clear priority for supporting economic growth. With inflation comfortably within its target range, and assuming favourable monsoon conditions, the central bank anticipates inflation to remain well-contained, contingent upon favourable domestic and global economic conditions.

Following two proactive repo rate cuts in 2025, a tangible and proportional reduction in borrowing costs is expected, paving the way for lower financing rates for real estate developers and end-users, potentially stimulating investments.

RBI’s shift from a 'neutral' to 'accommodative' stance signals focus on growth.

3. Developer Activity to Stay Strong

Upbeat momentum in developer land acquisition activity is likely to persist and even intensify in 2025 and beyond. Developers with strong balance sheets and a clear vision for future development will be particularly active in this space, especially across residential, built-up office, and mixed-use assets.

Top Investor’s Pick:

Core Sectors to Remain in Focus

- Residential and office sectors continue to dominate investor interest.

- India’s residential market is poised for stable growth in 2025 due to:

- Strong market fundamentals

- Rising appetite for homeownership

- Increasing disposable incomes

- Ongoing infrastructure development

- Elevated project launches expected, backed by ~USD 5.8 bn in land acquisitions during 2023–24.

- The office sector is set to grow further after two years of record leasing, driven by:

- Expansion by global and domestic occupiers

- Continued demand from the technology sector

- Growth from BFSI, engineering & manufacturing (E&M), and life sciences sectors

Promising Horizons in Alternate Sectors

- Alternate sectors remain attractive for investors with strong capital inflow projections.

- Data centres expected to see continued investment due to:

- Accelerated digital transformation across industries

- Strong policy support from central and state governments

- ~220 acres of land acquired in 2024 (15x YoY increase)

- ~USD 1 bn capital inflow into data centre development platforms in 2024

- The co-living sector is gaining traction due to:

- Rising cost of living

- Higher adoption of shared living arrangements among India’s young professionals

- Attractive returns and high growth potential

Quality assets take centre stage for investors

Sustainability on Investors’ Horizon

- Growing investor focus on sustainable and green developments

- ~20% of investors plan to acquire or develop green buildings, as per CBRE survey

- Rise in demand for high-quality sustainable workspaces in India

- Investors anticipate a modest premium for sustainable assets in the Indian market

Note: Equity investments in the real estate sector involve providing capital to acquire, develop, or operate real estate assets in exchange for a share of the ownership and the potential profits generated by those assets. Equity investments include those by private equity funds, pension funds, sovereign wealth funds. institutional investors, real estate developers, real estate fund-cum-developers, investment banks, corporate groups, and REITs, etc

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.