Press Release

Equity investments in realty sector set to hit a new record, crossing USD 10 billion in 2024

Institutional investors and developer companies to drive capital inflows

November 20, 2024

National – November 20th, 2024 – CBRE South Asia Pvt. Ltd., India’s leading real estate consulting firm released a report titled, ‘Leading the Charge: Crafting the Skylines of Tomorrow’. The report highlighted the real estate growth in India, key trends, and projections for the sector.

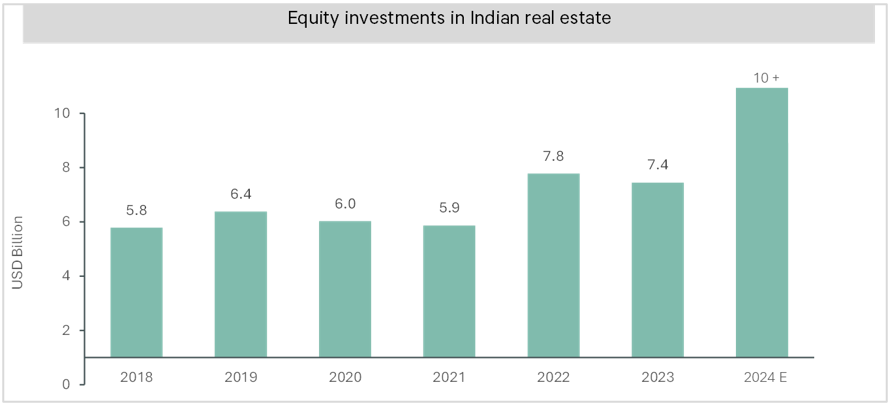

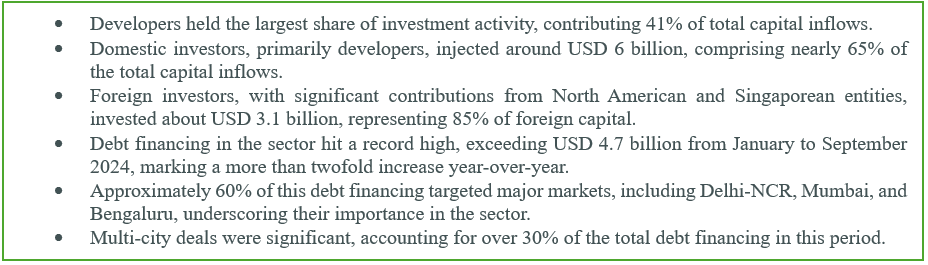

As per the report, overall equity investments in 2024 in the real estate sector are set to hit a new record surpassing USD 10 billion for the first time. With a resurgence in investment inflows in built-up office assets and a strong acquisition pipeline for land in the residential sector, overall equity investments in CY 2024 would be anticipated to be in the USD 10 – 11 billion range. This year, institutional and collective vehicle investors continued to be a major source of capital deployment in the Indian real estate sector, accounting for nearly 40% of the overall investments from January to September 2024. Developer companies led the total capital inflows with more than 41% share in this period. Domestic investors (predominantly developers) invested nearly USD 6 billion during the first nine months of the calendar year, dominating the overall capital inflows with an almost 65% share. In comparison, foreign investors contributed about USD 3.1 billion during the same timeframe. Notably, North American and Singaporean investors were the significant contributors, representing approximately 85% of all foreign capital inflows.

Equity capital inflows touched USD 8.9 billion between January and September, registering a 46% Y-o-Y growth. The strong momentum in deal volume continued, with about 200 deals reported during this period, compared to 151 deals in the same period last year. The average deal size also increased to nearly USD 45 million in the first nine months of 2024 from about USD 36 million in 2023. Mid-sized deals, ranging between USD 10-50 million, represented 56% of the total investment inflows during this period.

The office sector witnessed a resurgence of inflows during January-September 2024, with a nearly 50% Y-o-Y growth. Land/development sites and the office sector cumulatively attracted more than 70% of the investment flows during this period. Residential, retail, and mixed-use sectors also experienced a significant rebound in capital inflows, capturing a healthy share of the overall capital inflows in the first nine months of 2024. Nearly 64% of the capital inflows in the land/development sites went into residential developments, and the rest were allocated to mixed-use developments, warehousing projects, and the development of retail, data centre, and hospital projects.

Gateway cities such as Delhi-NCR, Mumbai, and Bengaluru remained the preferred markets with a cumulative share of over 63% in investment inflows in January-September 2024; Delhi-NCR witnessed the highest share of ~26% in capital inflows (amounting to ~USD 2.3 billion). Equity capital inflows into tier-II and III cities also reached nearly USD 0.6 billion, with Ludhiana, Mohali, Tuticorin, Hubli, Coimbatore, and Indore collectively accounting for ~76% of these inflows.

Debt financing in the real estate sector soared to a new peak in January-September 2024, surpassing USD 4.7 billion and marking a more than twofold increase compared to the same period last year. A significant portion of this financing, around 60%, was channelled into key markets such as Delhi-NCR, Mumbai, and Bengaluru, underscoring their pivotal role in the sector's growth. Moreover, the sector's adaptability was evident in the prevalence of multi-city deals, which accounted for over 30% of the total debt financing share.

Anshuman Magazine, Chairman & CEO - India, South-East Asia, Middle East & Africa, CBRE, said, "Projection for 2024 equity investments between USD 10 -11 billion, highest-ever, underscores continued investor interest in the growing real estate market in India. However, with SEBI's SM REIT framework, smaller but high-quality assets in tier-II markets will also present new avenues for strategic capital deployment. We believe this regulatory support will add much-needed transparency, enabling a more diversified investment base and encouraging institutional participation across these markets. Going ahead, this growing diversification will not only solidify India’s real estate sector but also pave the way for future growth across emerging asset classes."

Investment Outlook

• Equity Investment Forecast: Overall equity investments in India's real estate are projected to reach USD 10-11 billion in 2024, spurred by increased inflows in built-up office assets and a strong acquisition pipeline for land in the residential sector.

• Primary Markets: Metro and tier-I cities will remain the primary destinations for equity inflows, but SEBI’s SM REIT regulations would also create investment opportunities for high-quality, smaller assets in tier-II cities.

• Infrastructure Sector Growth: Private equity investments in public assets within infrastructure are expected to enhance accountability and operational efficiency.

• Healthcare Investment: Due to its capital-intensive nature, the healthcare sector is anticipated to attract stable, long-term capital inflows.

• Sustained Data Centre Investment: Investment momentum in data centres is anticipated to persist in the coming quarters.

• Renewables Sector Boost: A growing emphasis on sustainability is likely to drive more investments in the renewable energy sector.

• SEBI’s SM REITs Impact: SEBI’s SM REITs framework aims to bring greater transparency to the market, with CBRE estimating a potential market size in India of over USD 60 billion by 2026 .

• Long-Term Investment Strategies: Growth and controlling stake/buyout strategies reflect investors' long-term commitment to India's real estate market. The increasing deal volumes suggest a broader range of assets are securing debt and equity funding.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm (based on 2023 revenue). The company has more than 130,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves a diverse range of clients with an integrated suite of services, including facilities, transaction and project management, property management, investment management, appraisal and valuation, property leasing, strategic consulting, property sales, mortgage services and development services.

CBRE was the first International Property Consultancy to set up an office in India in 1994. Since then, the operations have grown to include more than 11,000 professionals across 15 offices, with a presence in over 80 cities in India. As a leading international property consultancy, CBRE provides clients with a wide range of real estate solutions, including Strategic Consulting, Valuations/Appraisals, Capital Markets, Agency Services, and Project Management. The guiding principle at CBRE is to provide strategic solutions that make real estate holdings more productive and economically efficient for its clients across all service lines. Please visit our website at https://www.cbre.co.in/